For decades, the global Indian entrepreneur operated under a straightforward, cross-border tax playbook. If you were an Indian citizen or a Person of Indian Origin (PIO) living abroad, you could fly into Mumbai, Delhi, or Bengaluru, spend a sizable chunk of the year managing your local ventures, catching up with family, attending board meetings, and as long as your stay didn’t hit the magical number of 182 days, your Non-Resident Indian (NRI) status remained completely safe. Your global income stayed out of the reach of the Indian tax authorities.

However, the global tax landscape has shifted dramatically. With changes introduced by the government in recent years, the cushion of the 182-day rule has worn thin for high-net-worth individuals (HNIs) and jet-setting promoters. In comes the 120-day residency rule—that broad legal net to snare any individual considered “stateless,” where he or she organizes residency among several countries to ensure no tax is paid at all, or who retains financial links to India despite residing overseas.

In today’s world, the global founders, fund managers, and multinational promoters are beginning to realize that they are “accidental residents” of India, which will create unexpected compliance issues, financial reporting issues, and corporate taxation issues.

The Genesis of the Trap: 182 Days vs. 120 Days

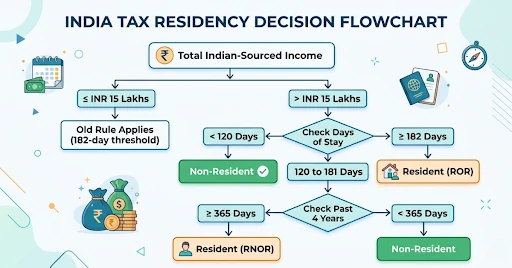

Under Section 6(1) of the Income Tax Act of 1961, historically, a person who stayed in India for at least 182 days in one financial year was considered a resident of the country. This generous exemption traditionally applied to all Indian citizens and Persons of Indian Origin (PIOs) visiting their homeland, offering them ample breathing room to manage domestic ventures without triggering complex Indian tax obligations.

This decades-old playbook was fundamentally rewritten during the presentation of the Union Budget on February 1, 2020. Introduced by the Union Finance Minister, Nirmala Sitharaman, the landmark Finance Act, 2020 amended these provisions to close loopholes used by highly mobile, affluent individuals. The new amendment officially went into effect on April 1, 2020 (applicable from the Financial Year 2020-21 onwards), specifically targeting individuals having a substantial financial interest in India by reducing the safe-harbor residency threshold from 182 days to 120 days under certain rigid criteria.

It is important to see how this provision can be applied. In order for an Indian citizen or a PIO who visits India to qualify as a resident, he should have:

- Their total income from Indian sources (excluding foreign income) exceeds INR 15 Lakhs during the financial year.

- Their physical stay in India is 120 days or more but less than 182 days.

- Their cumulative stay in India over the preceding 4 financial years is 365 days or more.

- If you hit this trifecta, you are no longer a Non-Resident. You are automatically categorized as a Resident but Not Ordinarily Resident (RNOR).

Why Jet-Setting Promoters are the Primary Target

The 120-day rule was specifically calibrated to capture individuals who run massive Indian operations from overseas or draw substantial income from domestic corporate ecosystems.

Consider a typical startup founder who relocated to Dubai or Singapore after a major funding round to handle global expansion. They continue to hold substantial equity in the Indian operational company, are part of the board of directors, and often visit India for business reviews, investor presentations, and marketing campaigns.

With all the activities such as attending board meetings and festivals on top of running the business, reaching the 120-day period in the financial year will occur much faster than anticipated. Since these promoters usually earn substantial dividends, sitting fees for directors, or interest income in India, the income earned in India will easily cross the 15 lakh rupees mark. Without realizing it, their calendar management fails them, and they land squarely in the “Accidental Resident” net.

Understanding Your Status: The Residency Matrix

| Category of Traveler | Indian Income Threshold | Stay in Current Financial Year | Cumulative Stay in Preceding 4 Years | Resulting Indian Tax Status |

| Standard NRI Traveler | Any Amount | Less than 120 Days | Any Duration | Non-Resident (NR) |

| High-Value Global Promoter | Exceeds INR 15 Lakhs | 120 Days to 181 Days | 365 Days or More | Resident but Not Ordinarily Resident (RNOR) |

| Frequent Short-Term Visitor | Exceeds INR 15 Lakhs | 120 Days to 181 Days | Less than 365 Days | Non-Resident (NR) |

| Deemed Resident (No Tax Base) | Exceeds INR 15 Lakhs | Any Duration (Stayed Abroad) | Not Liable to Tax Anywhere Else | Resident but Not Ordinarily Resident (RNOR) |

| Traditional Resident | Any Amount | 182 Days or More | Any Duration | Resident and Ordinarily Resident (ROR) |

Frequently Asked Questions (FAQs)

1. What exactly constitutes “Indian-sourced income” under the 120-day rule?

Income of an Indian origin is defined as the income that derives from sources in India. In case of the promoters, this may include payments like dividend income from Indian companies, salaries from services provided in India, director’s fees, rents from properties situated in India, capital gains from sales of Indian shares and property. Significantly, it does not include income generated from abroad from foreign assets or business or from foreign employment.

2. If I become an RNOR due to the 120-day rule, will India tax my global income?

No, all your worldwide income will not be immediately subject to tax. You benefit from the RNOR status for the time being. Under the RNOR status, the foreign sourced income of an individual is exempt from taxes in India, provided the business/profession is not controlled/formed within India.

3. What is the biggest trap if my status changes to RNOR?

The biggest trap isn’t always immediate taxation; it is compliance, scrutiny, and corporate exposure. If your foreign business is deemed to be “controlled from India” because you spent over 120 days in the country making executive decisions, that foreign business’s income could face Indian taxation. Moreover, getting included in the residential taxation tax regime entails a high reporting responsibility.

4. Can a change in personal residency status impact my overseas company?

Indeed, a lot. And that’s when Place of Effective Management (POEM) regulations kick in. In case a promoter is an Indian resident and he is managing a foreign entity from India while he is there for over 120 days, then the tax officials can claim that the POEM of the foreign firm lies in India. If proven, all the income earned worldwide by the foreign firm would be taxed under the Indian corporate tax regime.

5. Does the 120-day rule apply if my Indian income is exactly INR 15 Lakhs?

Absolutely not. This is clearly stated in the law, that the aggregate income arising from India should be more than INR 15 Lakhs. If your Indian-sourced income is INR 15 Lakhs or less, the old 182-day threshold continues to apply to you, regardless of how many days you spent in India (provided you don’t hit standard residency criteria).

6. How does the “Deemed Residency” rule tie into this?

A provision of the Finance Act also includes a term known as “deemed resident.” According to this clause, an Indian citizen, who earns income from India in excess of INR 15 Lakhs but is not taxable as a resident in any other foreign country on account of domicile or residence, will be considered an Indian resident (i.e., RNOR).

7. How are the number of days calculated? Do arrival and departure days count?

Of course, in calculating the number of days of stay within the country, the very day when the taxpayer enters or leaves the country is considered as a complete day of stay for the purposes of income tax computation under the Indian Income-tax Act. This is something that promoters who follow their movements based on their passports should be aware of.

8. How can a promoter protect themselves from becoming an accidental resident?

Promoters must strictly maintain a comprehensive physical stay calendar, ensuring they stay well under 119 days if their Indian revenues are high. Alternatively, they must ensure that strategic management decisions (such as signing contracts, holding global board meetings, and hiring executives for foreign operations) are strictly conducted while they are physically outside India to avoid POEM triggers.

The Domino Effect on Corporate Structuring and Compliance

Being an accidental resident is not only a matter of individual taxation but results in operational issues as well. Once the promoter finds himself inadvertently in this position, his ability to use particular non-resident banking instruments, like NRE accounts, will also change. As per the FEMA guidelines, whose definition of residency differs slightly yet focuses on intent, the long-term presence can lead to complications in the transfer of funds.

In addition to this, tax authorities have used sophisticated techniques for data analysis. With the help of comparing the immigration data (Immigration Bureau data) with Ministry of Corporate Affairs (MCA) data and bank transactions, it becomes easy for the tax department to identify the persons who were spending substantial time in India despite having major promoter/managerial holdings.

Conclusion

Managing tax obligations in a cross-border scenario entails much more than merely counting your number of calendar days. We at RAAAS help international businesses as well as ultra-high-net-worth individuals develop a strategic India Entry Strategy to protect themselves from regulatory pitfalls while achieving maximum growth opportunities. Are you planning to expand your presence internationally through setting up a new Foreign Entity in India? We can help you with that through our comprehensive services ranging from Foreign Company Incorporation in India to managing Foreign Entities in India. Our range of premium services for your company includes advisory for Company Setup in India and Company Establishment in India along with the Registration of Foreign Companies in India.

Further, our premium tax advisory services help protect your promoters from becoming unintentional tax residents while achieving operational efficiency through our dedicated solutions such as SAP Outsourcing and Accounts Outsourcing for Startups. Partner with us to seamlessly scale your business across borders while ensuring your corporate health and compliance stand firm.