Understanding GST and Valuation Rules for Related Parties: A Comprehensive Guide

Introduction:

In the dynamic landscape of business transactions, relationships between related parties play a pivotal role in shaping economic activities and driving growth. However, when it comes to taxation, especially under the Goods and Services Tax (GST) regime, these transactions between related parties necessitate a thorough understanding of valuation rules to ensure compliance and fair treatment.

Welcome to our comprehensive guide on “Understanding GST and Valuation Rules for Related Parties.” In this guide, we will delve into the intricate world of GST and explore the nuanced valuation rules that govern transactions between related parties. Whether you’re a business owner, tax professional, or simply seeking clarity on this complex subject, this guide aims to provide you with a comprehensive understanding of the regulatory framework, compliance requirements, and best practices associated with related party transactions under the GST regime.

As we embark on this journey, we will unravel the definitions, types, and significance of related party transactions, laying the groundwork for a deeper exploration into the application of GST and valuation principles. From understanding the arm’s length principle to navigating the specific valuation rules outlined under the GST law, we will examine the intricacies involved in determining the taxable value of goods and services exchanged between related parties.

Furthermore, we will address the compliance challenges and practical considerations that businesses encounter when engaging in related party transactions under the GST regime. Through real-world examples, best practices, and expert insights, we aim to equip you with the knowledge and tools necessary to navigate this complex terrain with confidence and clarity.

In a rapidly evolving regulatory landscape, staying abreast of GST laws and valuation rules is essential for businesses to ensure compliance, mitigate risks, and optimize tax outcomes. Whether you’re seeking to enhance your understanding of related party transactions or seeking practical guidance on GST compliance, this guide serves as your go-to resource for comprehensive insights and actionable strategies.

Join us as we embark on a journey to unravel the intricacies of GST and valuation rules for related parties, empowering you to navigate this complex landscape with clarity and confidence. Let’s dive in!

Understanding Related Party Transactions:

Definition of Related Parties:

Related parties are entities or individuals that have the ability to control, influence, or exercise significant power over one another. These relationships can arise due to various factors, including ownership, common control, or significant influence.

Key Characteristics of Related Parties:

- Control: Related parties often share a common control structure, where one entity has the power to govern the financial and operating policies of another entity. Control can be exerted through ownership of voting rights, contractual agreements, or other mechanisms.

- Influence: Related parties may exert significant influence over one another, even in the absence of direct control. This influence can stem from familial relationships, business partnerships, or other connections that enable one party to sway the decisions or actions of another.

- Economic Dependence: Related parties may be economically dependent on each other, relying on mutual support or collaboration to achieve their financial objectives. This dependence can manifest in various forms, such as shared resources, joint ventures, or intercompany transactions.

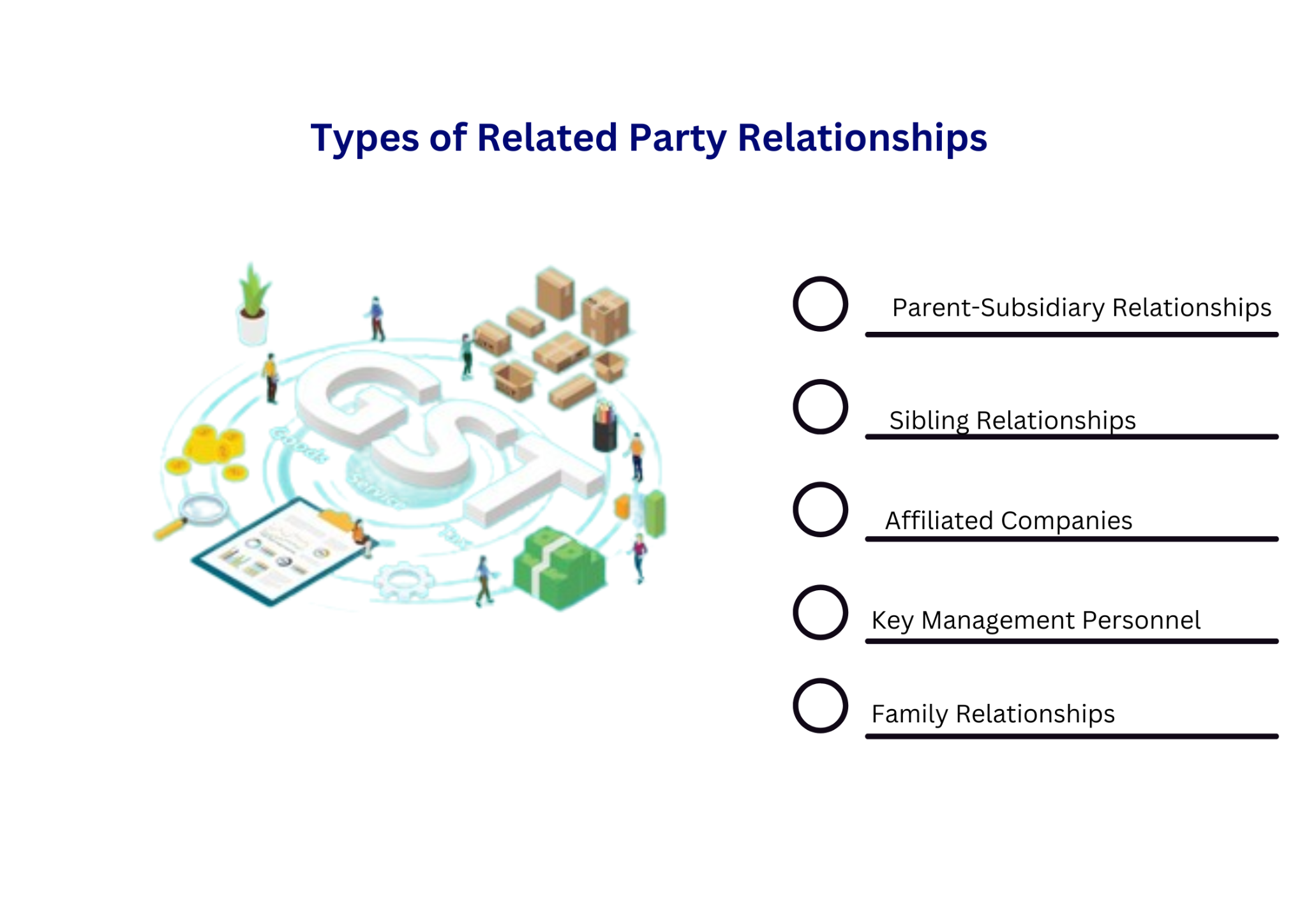

Types of Related Party Relationships:

- Parent-Subsidiary Relationships: A parent company typically holds a controlling interest in its subsidiary, allowing it to govern the subsidiary’s operations and financial policies.

- Sibling Relationships: Sibling entities refer to companies that share a common parent or have a significant level of common ownership but operate as separate legal entities.

- Affiliated Companies: Affiliated companies are entities that are related through common ownership or control, often engaging in collaborative activities or sharing resources to achieve common goals.

- Key Management Personnel: Individuals in key management positions, such as executives, directors, or significant shareholders, may be considered related parties due to their influence over the entity’s decision-making process.

- Family Relationships: Related parties can also include family members of key stakeholders, such as spouses, children, or siblings, who may have a direct or indirect impact on the entity’s affairs.

Importance of Identifying Related Parties:

Accurately identifying related parties is crucial for financial reporting, taxation, and regulatory compliance purposes. Disclosure of related party transactions is required under accounting standards to ensure transparency and fair representation of an entity’s financial position and performance.

Furthermore, related party transactions may be subject to scrutiny by regulatory authorities to prevent conflicts of interest, ensure fair pricing, and maintain the integrity of financial statements. By understanding the definition and characteristics of related parties, businesses can navigate related party transactions with greater transparency, accountability, and compliance with regulatory requirements.

GST and Related Party Transactions:

- Applicability of GST: Related party transactions are subject to GST if they involve the supply of goods or services for consideration in the course of business or furtherance of a business.

- Valuation of Goods and Services: GST is levied on the transaction value of goods or services. However, in related party transactions, the transaction value may need to be determined based on specific valuation rules to ensure compliance with the arm’s length principle.

Valuation Rules for Related Party Transactions under GST:

- Rule 28 of the CGST Rules, 2017: This rule provides guidance on determining the value of goods or services in related party transactions when the transaction value is not ascertainable due to certain circumstances.

- Comparison with Open Market Value: The valuation rules may require comparing the transaction value with the open market value of similar goods or services to arrive at a fair and reasonable value for GST purposes.

- Documentation and Record-Keeping: Maintaining proper documentation and records of related party transactions is essential for demonstrating compliance with GST valuation rules.

In the GST regime, determining the value of supply is essential for taxation purposes. Section 15(4) of the CGST Act empowers the government to prescribe rules for valuation in specific situations. Let’s explore these rules through examples and case studies.

Rule 27: Value of Supply Not Wholly in Money

When the consideration for a supply is not wholly in money, the value shall be determined as follows:

Example 1:

- A laptop is supplied for Rs. 30,000 along with an exchange of an old laptop. The open market value (OMV) of the new laptop without exchange is Rs. 36,000. The value of supply will be Rs. 36,000 (OMV).

Rule 28: Value between Distinct or Related Persons

For supplies between distinct or related persons, the value shall be:

Example 2:

- TATA Steel supplies goods worth Rs. 2,50,000 to TATA Motors for Rs. 2,00,000. TATA Motors claims full input tax credit of Rs. 36,000. The invoice value of Rs. 2,00,000 shall be deemed the open market value.

Rule 29: Value of Supply through an Agent

The value of supply between principal and agent shall be the open market value or 90% of the price charged for the supply of like goods by the recipient to an unrelated customer.

Example 3:

- A principal supplies leather wallets to an agent. The agent sells wallets to customers at Rs. 2,000 each. The value of supply by the principal will be Rs. 1,800 (90% of Rs. 2,000).

Rule 30: Value Based on Cost

If the value cannot be determined by previous rules, it shall be 110% of the cost of production or acquisition.

Example 4:

- XYZ Limited manufactures office chairs at Rs. 4,000 per chair. The open market value is Rs. 4,500. The value will be Rs. 4,400 (110% of cost) if open market value is not available.

Rule 31: Residual Method

If value cannot be determined by previous rules, it shall be determined using reasonable means consistent with GST principles.

Example 5:

- When cost of production cannot be determined, the number of man-hours required for a job can be used for valuation.

Rule 31A: Value in Specific Supplies

For lottery, betting, gambling, and horse racing, specific valuation methods are prescribed.

Example 6:

- For the lottery, the value is deemed to be a certain percentage of the face value of tickets, as notified by the organizing state.

Rule 32: Determination of Value in Certain Supplies

Specific valuation methods are provided for certain supplies, such as exchange of foreign currency.

Example 7:

- For the exchange of foreign currency, the value of supply is determined based on the buying or selling rate of the currency.

Compliance and Challenges:

- Compliance Requirements: Businesses engaging in related party transactions must ensure compliance with GST laws and valuation rules, including timely payment of GST and accurate reporting of transactions.

- Challenges in Valuation: Determining the appropriate valuation of goods or services in related party transactions can pose challenges due to the subjective nature of valuation and the need to satisfy the arm’s length principle.

Best Practices and Recommendations:

- Transparent and Adequate Documentation: Maintain comprehensive documentation of related party transactions, including contracts, invoices, and supporting documents, to facilitate accurate valuation and compliance with GST regulations.

- Professional Advice: Seek guidance from tax experts or consultants familiar with GST laws and valuation principles to ensure proper compliance and mitigate risks associated with related party transactions.

Frequently asked questions

Q.1) What are the key considerations for determining the transaction value under GST for related party transactions?

Answer: The transaction value under GST for related party transactions should reflect the price actually paid or payable for the supply of goods and/or services. It should include all relevant considerations, such as taxes, incidental expenses, amounts for which the supplier is liable, and any subsidies directly linked to the price. Additionally, it’s crucial to ensure that the valuation adheres to the arm’s length principle to avoid any potential disputes with tax authorities.

Q.2) How does the GST valuation differ for related party transactions compared to transactions between unrelated parties?

Answer: In related party transactions, there’s a higher scrutiny to ensure that the transaction value reflects the fair market value or the value that would be determined between unrelated parties (arm’s length principle). This is to prevent any potential abuse of transfer pricing or undervaluation of goods or services exchanged between related parties for tax purposes.

Q.3) What are the documentation and compliance requirements for related party transactions under GST?

Answer: For related party transactions under GST, it’s essential to maintain comprehensive documentation to substantiate the transaction value, including contracts, invoices, transfer pricing studies (if applicable), and any other relevant records. Additionally, businesses should ensure compliance with GST regulations related to related party transactions, including disclosure requirements in GST returns and any additional reporting obligations.

Q.4) How can businesses ensure compliance with GST valuation rules for related party transactions?

Answer: Businesses can ensure compliance with GST valuation rules for related party transactions by conducting thorough due diligence to determine the arm’s length price, documenting the rationale behind the valuation, maintaining accurate records, and obtaining professional advice when necessary. Implementing robust transfer pricing policies and procedures can also help mitigate the risk of non-compliance.

Q.5) What are the implications of non-compliance with GST valuation rules for related party transactions?

Answer: Non-compliance with GST valuation rules for related party transactions can result in penalties, interest, and potential tax assessments by tax authorities. Additionally, it may lead to reputational damage and legal consequences for the business. Therefore, it’s essential for businesses to proactively ensure compliance with GST regulations to mitigate these risks.

Conclusion:

Navigating related party transactions in the context of GST requires a thorough understanding of valuation rules, compliance requirements, and best practices. By adhering to the principles of transparency, documentation, and seeking professional advice when needed, businesses can effectively manage the complexities associated with related party transactions under the GST regime.

Through this comprehensive guide, we hope to provide businesses with valuable insights and practical guidance to navigate the nuances of GST and valuation rules concerning related party transactions, enabling them to ensure compliance and enhance their business operations in a tax-efficient manner.